What it actually takes to turn fragmented data into deposits, a recap of the From Record to Revenue panel, and why the recording is worth an hour of your time.

Most banks and credit unions aren't struggling because they lack data. They're struggling because the data they have isn't usable by the teams who need it most.

The short answer: most institutions already have the data they need. What they're missing is a unified layer between their systems of record and their marketing tools, a nd a data model in HubSpot built to reflect the complexity of real financial relationships. This post breaks down the framework and the real outcomes from institutions that have done it.

That was the through-line of From Record to Revenue: How Financial Institutions Turn Data into Deposits, a panel discussion hosted by GreenHouse Agency and iDENTIFY that brought together practitioners from five organizations, including marketing and BI leaders from Sound CU and Old Glory Bank, to talk candidly about what it actually takes to fix a fragmented data problem, and what becomes possible when you do.

This is a recap. It won't give you everything, including the full story of how one credit union recovered over $17 million in loans and deposits in ten months. But it should give you a sense of whether the full session is worth your time.

Why Financial Institution Data Doesn't Work for Marketing Teams

Data fragmentation isn't a new problem in financial services. Core systems, loan origination platforms, digital banking tools, onboarding systems, fintech integrations, the average institution is juggling a stack that was never designed to talk to itself.

The result is that teams are being asked to grow deposits, increase share of wallet, and deliver personalized experiences while working from an incomplete picture of the customer or member they're trying to reach.

Lee Easton, President of iDENTIFY, named what many teams already know but rarely say: the assumption that the data coming out of those separate systems is consistent, or even clean, is one of the most expensive misconceptions in the industry. Fields go missing. Zip codes get mapped into name fields. A vendor sends clean records for 30 days, then doesn't. If your CRM is built on top of that without a validation layer, every subsequent campaign inherits those problems.

This is the silent cost. Not just bad reporting, but bad targeting, missed opportunities, and compliance risk built into the foundation.

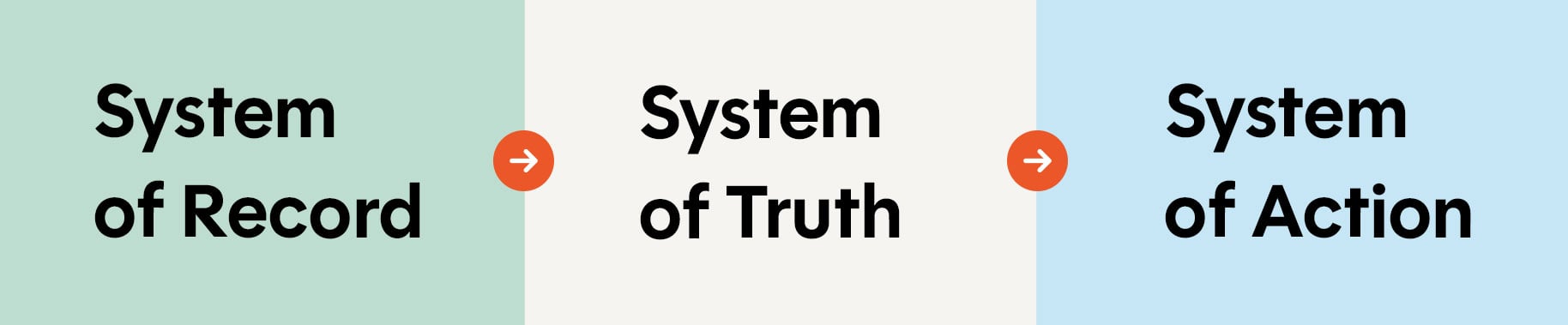

The Three-Layer Data Framework: System of Record, Truth, and Action

The panel organized the solution around three distinct layers that came up across every example in the session.

System of Record, where your data actually lives: core platforms, LOS, digital banking, and warehouse. This layer isn't going away and shouldn't be replaced. It's the foundation.

System of Truth, where data gets cleaned, unified, and trusted. This is where most institutions stall. Justin Buys, Director of Development at GreenHouse Agency, noted that hearing "data warehouse" from someone on the IT side is a signal of a more mature data foundation; it means the institution has started unifying data across systems and there's something to build on.

System of Action, where teams can finally use what they know. For most institutions, this is where HubSpot enters the picture. And this is where the session got concrete.

Watch the Full Webinar

What a HubSpot Data Model for Financial Institutions Actually Looks Like

A Lead Services Consultant from HubSpot's financial services team was direct about what makes financial institutions structurally different from the companies HubSpot was originally built for: the data model has to represent a richer set of relationships.

A standard out-of-the-box CRM setup flattens the member or customer relationship into something that loses most of its value. A member might have a checking account, a savings account, an auto loan, a credit card, and a pending mortgage application. If your CRM treats that person as a single contact record with aggregate fields, you can do some things, but not the right things.

The goal is a data model that surfaces individuals and all of their distinct financial relationships with your institution, products, accounts, applications, pre-approvals, and behavioral signals from digital banking, so that marketing, lending, and service teams are looking at the same complete picture. Not a flattened version of it.

HubSpot for financial institutions isn't about replacing the system of record. It's about building a usable operating layer across the fragmented systems that already exist and aren't going anywhere.

What This Looks Like in Practice

This is where the session shifted from framework to reality, and it's the part worth watching in full.

Amy Shuey, VP of Marketing and Payments at Sound CU, walked through what her team built after creating a MeridianLink integration with HubSpot. Before the integration, non-member loan applications were essentially invisible inside HubSpot. After her team built automated workflows across every loan type, credit cards, auto loans, personal loans, business lines of credit, with a three-email abandoned application sequence that runs without marketing having to touch it. Four recovered loans covered the HubSpot subscription for the year. Everything else is upside down.

creating a MeridianLink integration with HubSpot. Before the integration, non-member loan applications were essentially invisible inside HubSpot. After her team built automated workflows across every loan type, credit cards, auto loans, personal loans, business lines of credit, with a three-email abandoned application sequence that runs without marketing having to touch it. Four recovered loans covered the HubSpot subscription for the year. Everything else is upside down.

John Kingma, CTO and CISO at Old Glory Bank, described moving nearly 100,000 prospects from a reservation list through a structured onboarding journey in a matter of months. A direct deposit campaign built on the same data foundation generated over $8 million in new deposits. Business account openings grew more than 300% year-over-year after refining the triggers and workflows.

reservation list through a structured onboarding journey in a matter of months. A direct deposit campaign built on the same data foundation generated over $8 million in new deposits. Business account openings grew more than 300% year-over-year after refining the triggers and workflows.

These aren't projections. They're outcomes from institutions in production.

The Change Management Problem

One of the best questions from the live audience was about organizational alignment, a recurring theme in HubSpot adoption in financial services, specifically, how to bring along departments still operating in old ways.

Amy's answer was direct: do it, and they'll catch up. When results are visible, buy-in follows.

John's lesson was more foundational: he would have invested in the data layer sooner. The temptation is to move quickly to campaigns and workflows, but the strongest outcomes come from normalizing and harmonizing data first, then building on top of something solid. The cultural friction is real, but it moves when the results are visible, reduced friction for the member or customer, efficiency gains in the back office, and clear ROI.

What This Recap Can't Give You

It doesn't give you the actual HubSpot workflow screenshots that Amy and John walked through live. It doesn't give you the Q&A, which ran five minutes over because the questions were too good to cut. And it doesn't give you the HubSpot consultant's framework for the first 90 days of a HubSpot implementation, the MVP rollout approach that starts with one or two high-impact use cases instead of trying to rebuild every journey at once.

One credit union referenced during the session used a real-time abandoned application journey to recover over $17 million in loans and deposits in ten months. That example, and the thinking behind it, lives in the recording.

If your institution is managing disconnected systems while being asked to grow, this session was built for you. The practitioners on the panel are doing this work right now, not in theory.